Introduction

This guide provides information pertaining to the requirement and procedure for registration under the Goods and Services Tax Act (GST). It is recommended that you read the GST General Guide before reading this guide as this guide requires a fair understanding of the general concept of GST.

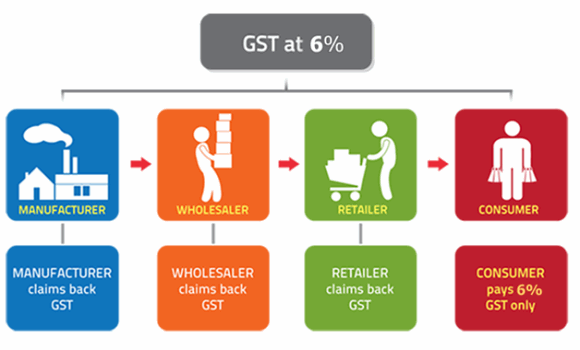

Goods and Services Tax (GST) is a multi-stage tax on domestic consumption. GST is charged on all taxable supplies of goods and services in Malaysia except those specifically exempted. GST is also chargeable on the importation of goods and services into Malaysia.

Payment of tax is made in stages by the intermediaries in the production and distribution process. Although the tax would be paid throughout the production and distribution chain, it is ultimately passed on to the final consumer. Therefore, the tax itself is not a cost to the intermediaries and does not appear as an expense item in their financial statements.

In Malaysia, a person who is registered under the Goods and Services Tax Act 201X is known as a registered person. A registered person is required to charge output tax on his taxable supply of goods and services made to his customers. He is allowed to claim input tax credit on any GST incurred on his purchases which are inputs to his business. Thus, this mechanism would avoid double taxation and only the value added at each stage is taxed.